-

Software Products

-

Loan Software

Loan Software -

Banking Software

Banking Software -

Real Estate Software

Real Estate Software -

Self-Help Group(SHG)

Self-Help Group(SHG) -

NBFC Software

NBFC Software -

Nidhi Companies

Nidhi Companies -

RD FD Software

RD FD Software -

Pigmy Software

Pigmy Software -

Mortgage Software

Mortgage Software -

Microfinance Software

Microfinance Software -

Core Banking Software

-

Micro Small and Medium

-

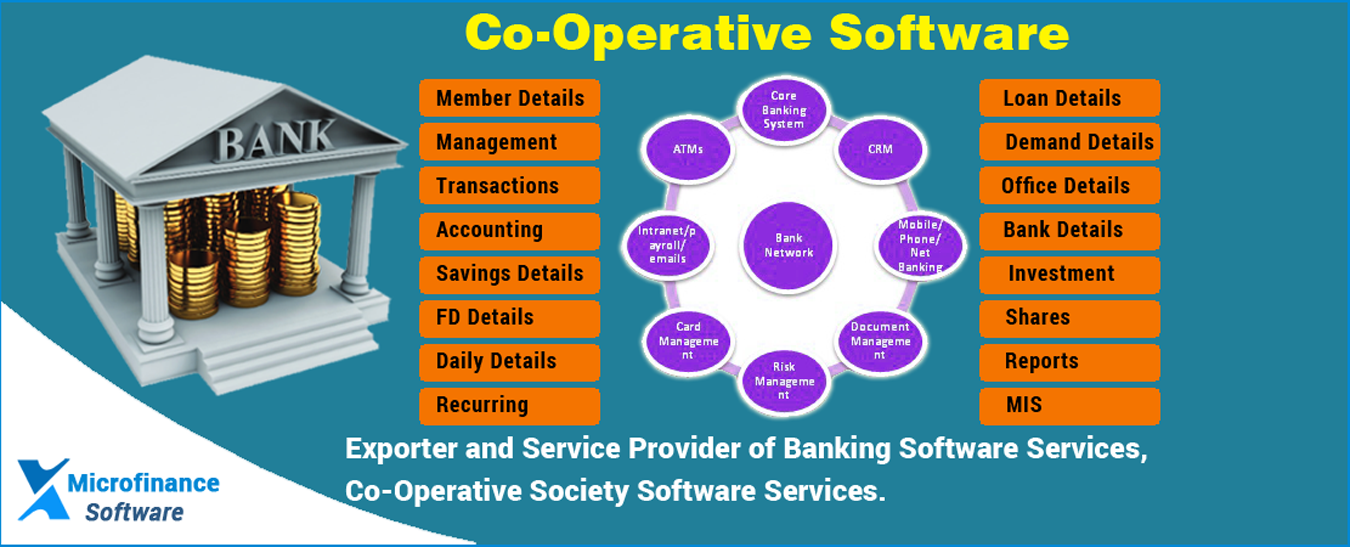

Co-Operative Software

Co-Operative Software -

Daily Collection Software

Daily Collection Software -

Custom finance Software

Custom finance Software -

Merchant finance Software

-

Vehicle Loan Software

Vehicle Loan Software - Gold Loan Software

- Micro Small Enterprises

-

Trust Software

Trust Software - Producer Company

-

Principles of Microfinance

1. The poor need a variety of financial services: The Bank will support demand-driven microfinance interventions that develop and provide financial services.

2. Microfinance is a powerful instrument against poverty: The Bank will ensure that its operations support initiatives that increase the access of people in RMCs who are presently excluded from accessing quality financial services.

3. Microfinance means building financial systems that serve the poor: The Bank will support its RMCs to build such systems.

4. Financial sustainability is necessary to reach significant numbers of poor people: The Bank will support initiatives that help suitable intermediaries achieve financial self-sufficiency.

5. Microfinance is about building permanent local financial institutions: Dependence on concessional funding from such agencies as the Bank will only be temporary and diminish over time. The support of microfinance by the Bank will be contingent on intermediaries that are progressing toward, if they have not already attained, financial self-sufficiency.

6. Microcredit is not the only answer: In supporting microfinance in it’s the RMCs, the Bank will consistently establish that any resources applied to target groups and identified as credit will be extended through a viable institutional intermediary with a clear means of repayment at market rates of interest.

7. Interest rate ceilings debilitate the ability of all, but especially the poor, to access financial services: The Bank will support the ability of all RMC financial intermediaries to charge market rates of interest on loans. The Bank will further support the elimination of interest rate ceilings and the creation of more operational efficiencies to reduce MFI costs, thereby allowing them to reduce the rates of interest charged on loans.

8. Governments are to act as enablers, not as direct providers of financial services: The Bank will support RMC governments in defining the elements of the enabling environment necessary to mainstream microfinance into the formal financial sector. At the same time, the Bank will discourage RMC governments from directly funding people targeted by MFIs.

9. Funding agencies should complement, not compete with, private-sector capital: The Bank will provide selective support for initiatives with the objective of building inclusive financial systems. The Bank will, however, require a defined exit strategy at the outset of such support.

10. The absence of institutional and human resource capacity is the key constraint: The Bank will support building the institutional capacity of financial intermediaries to provide financial services in demand among people who do not have access to formal financial services.

11. Transparency in financial and outreach matters is important: Bank support to microfinance in the

RMCs will help ensure transparency at all levels and by all institutions.

Testimonials

" Very Thanks to Microfinancesoftware for creating such a useful product. It has streamlined

and enhanced the quality of our service and it is very good to expand the business."

Software Demo

Promos

Our Clients

Products

►NBFC

►Mortgage

►Merchant Finance

►Vehicle Loan

►Gold Loan

►Micro Small Enterprises

►Custom Finance

Skype

Download Skype Click to Call is a

really easy way for you to make

calls to numbers on websites

Download Team Viewer 9.0 and

connect your desktop to other computer

Download Ammyy 3.5 and connect

your desktop to other computer

WITH US